Goal of this story

- Define Fraud and Payment risk and “WHO” is impacted?

- Payment risk and fraud — what’s the difference!

- Fraud prevention tools and technologies

- Innovation happening in this space

So let’s begin!

WHY we all should be aware of Digital Payment risk and Fraud!

Cardholder story

I recently got an email and a call from Financial institution to inform that they will issue me a new credit card (replacing the existing one) and when I asked why are you doing this they said they noticed “some suspicious fraud activity” on my account and they think to replace the card can prevent that.

Bank account holder story

This is nothing, my friend recently got a message alert that some amount is being deducted from the account and he had no clue how did this happen!!!

Business owners and Merchants story

Online merchants know very well that fraud costs them in many ways — in chargebacks, in false positives, in the friction that’s introduced at checkout that can cost a sale. Source

Financial Institution side of story

According to an IBM Institute for Business Value (IBV) study of 500 bank C-level executives, many legacy fraud systems are perceived as hard to adapt to new, faster and changing cross-channel threats. 81% of respondents said it takes more than four weeks to discover a new pattern, then another four weeks to adjust the scoring engines.

So by now, you would have understood that Digital payment fraud impacts everyone from Consumers to Merchants to Financial institutions!!

And the first thing that we all can do to prevent this is to make ourselves aware of the payment fraud and Risk ecosystem. Know it and understand it because it deals with money!

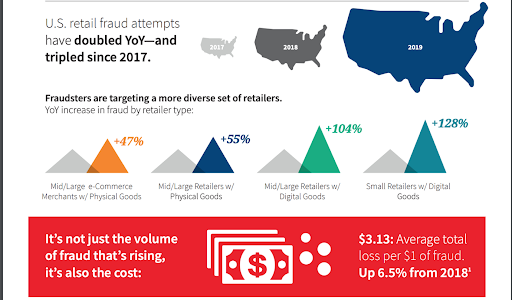

So how much it costs is the next question.

According to Juniper Research, online and mobile payment fraud is being fueled by identity and payment information stolen through the ongoing epidemic in data breaches. The firm estimates losses from online payment fraud will top $22 billion this year — and could go as high as $48 billion by 2023.Source

While technology is helping merchants with new channels for doing business with ease and speed, it also introduces cost to them due to payment risk and fraud❗

Now let’s understand what is the Payment Risk and Fraud

In a typical, cash transaction between Merchant and consumer the chances of Fraud happening is less as the money flow is happening between 2 parties. This means there is a low payment Risk.

With Online credit card transaction, apart of merchant and consumers, there are many other entities gets involved and in such cases, money flow can be risky as there are high chances of fraud. So, in this case, the payment transaction is at high risk.

So it all depends on the companies business and their policy, the higher the risk, the higher the fraud prevention tools need to be there.

The more information available to verify the identity of the user the less risky the payment would be.

How do frauds happen?

Our ability to manufacture fraud now exceeds our ability to detect it.

Al Pacino

The fraudsters can be an individual or part of a big organization who will continuously acquire data via malware, hacking or some means of buying the data from external sources who will then validate the data and will try to predict the complex identity of certain individual. This can lead to Identity takeover!!

fraudsters can then make purchases for such stolen identities. This ultimately results into Fraud!

There are other ways as well through which Fraud happens, viz.

- Business E-Mail Compromise

- Denial of Service

- Phishing/Spoofing

- Ransomware

- Social Engineering

What solutions are currently available to combat fraud?

In the case of Card present transaction, Merchants do not have to bear much cost other than the chargebacks or order processing. In this case, Card associations are protecting Merchants for any fraud. Here, card and its identity can be immediately verified/authenticated through the point of sale terminals.

But…With the growing popularity of online commerce, it is very difficult for merchants to not have their presence there. Ultimately their sales are increasing with the online presence. At the same time Merchants will have to ensure their infrastructure is secured and the possibility of Fraud happening is less.

Research says the rate of online fraud to be approximately seven times that of fraud in the card-present world. Some independent analysts have the estimate as high as twelve times.

There are Fraud prevention tools available to online Merchants now which can help them know if the order is Risky or not risky. These tools will be based on rules which will be configured for each merchant type and as per their business model. There are times when Merchants are willing to take some risk on orders which are flagged as risky. This is done so that merchants can give a good customer experience and build a loyal customer base.

There are other solutions like Multi-factor authentication available which is bringing friction in the checkout process but to some extent helping merchants from preventing frauds.

“We are giving away too much biometric data. If a bad guy wants your biometric data, remember this: he doesn’t need your actual fingerprint, just the data that represents your fingerprint. That will be unique, one of a kind.” — Mike Muscatel, Senior. Information Security Manager, Snyder’s-Lance.

What next! Innovations through technology!

With AI ( Artificial Intelligence) and ML ( Machine Learning) technologies, there are companies who are able to build ML-based models which are built by collecting data about the users’ physical attributes, digital attributes and behavioral pattern so that Identity can be verified and fraud can be prevented.

Innovation can come with Supervised and Unsupervised Learning ( Machine Learning) based Models which most of the companies are focussing on!!

“Blockchain technology has broad implications for the commercial payments space, from speeding up settlements to securing cross-border transactions,” said Rick Burke, Head of Corporate Products and Services at TD Bank. Source

Conclusion

While there are technology innovations happening to combat Fraud, it is important for online merchants to be more aware of the cybersecurity and build a robust technology infrastructure using ML, Automation. This would certainly prevent fraud to some extent.